Diversification

Not a Free Lunch, But a Great Meal

The previous articles in this series established a foundation for Portfolio Thinking’s approach to investing; we will now start building on that foundation by applying those principles. In other words, we are moving from the ‘thinking’ to the ‘portfolio’. In this context, a ‘portfolio’ is a collection of assets carefully designed to meet the investor’s financial goals.

Before focusing on how we build a portfolio, it is worth reminding ourselves why we need one, rather than simply holding a single asset, and what it is ultimately designed to achieve.

At its heart, a portfolio approach is an attempt to harness the benefits of diversification. Nobel laureate Harry Markowitz famously called this “the only free lunch in investment”. While I hesitate to disagree with Markowitz, this is not strictly true.

An investor who could correctly identify the absolute best asset and hold it for the duration of their investing career would achieve the highest possible returns. By investing in other assets, we naturally dilute the returns of that single ideal asset. Consequently, a portfolio is, by its very nature, a sub-optimal investing strategy. However, the probability of successfully selecting and holding the “best” asset over an entire lifetime is so minuscule that this ‘sub-optimal’ approach ultimately becomes the superior strategy.

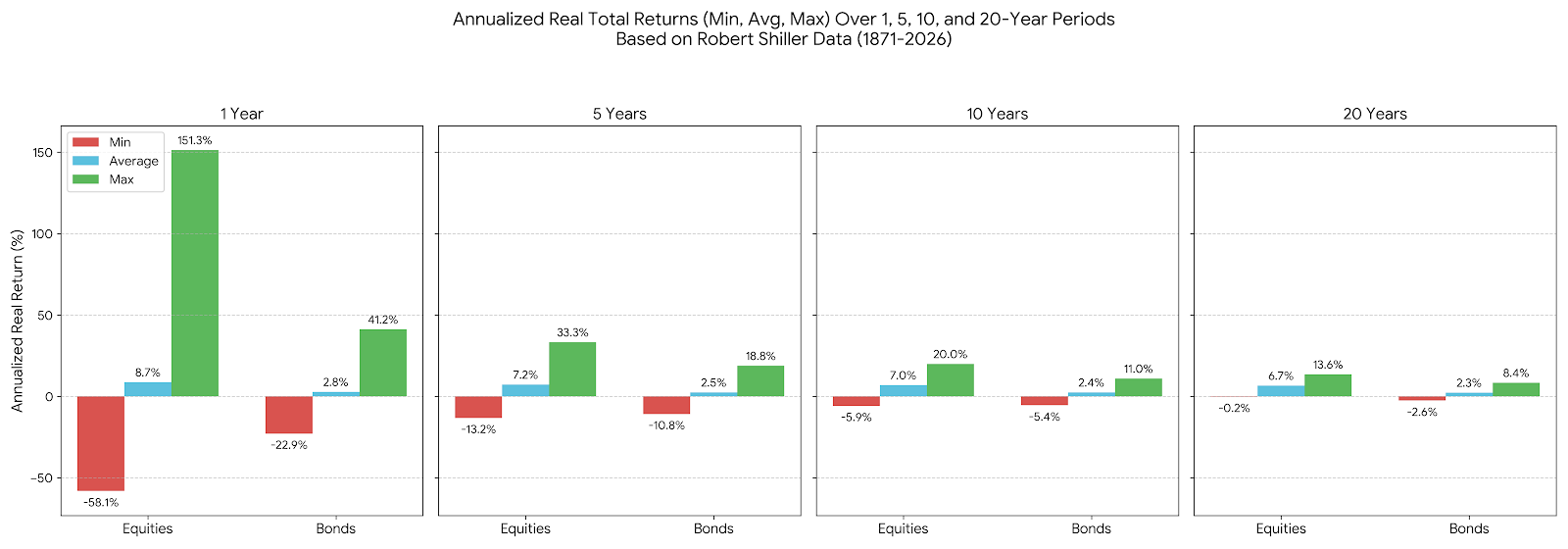

Even if we move from the single-asset level (e.g., a specific company) to the broad asset-class level (e.g., US equities), we can see both the sub-optimal nature and the distinct benefits of a diversified portfolio. This is illustrated in Figure 1, which details the minimum, average, and maximum real (after-inflation) returns of US equities, and bonds over rolling 1, 5, 10, and 20 year periods since 1871. This data clearly demonstrates that over a reasonable investment horizon, equities deliver significantly higher average returns than bonds. Therefore, including bonds inevitably dilutes peak returns, limiting the overall absolute gain.

The Psychological Edge

However, these returns are not accumulated evenly. While the gap between minimum, average, and maximum returns narrows as the investment time horizon lengthens, equities have produced negative (real) returns across all investment periods measured.

These negative periods create a profound psychological challenge: as investors, we feel the pain of a ‘loss’ approximately twice as intensely as we feel the joy of a ‘gain’. Consequently, the more frequently we observe a loss, the harder it is to stay on track toward our goals, increasing the likelihood that we will abandon our strategy and sell.

Using long-term data, we can estimate how often an investor will feel the sting of a loss based purely on how frequently they check their portfolio.

Probability of Observing a ‘Loss’ in an Equity Portfolio

1 Day: 48.61%

1 Week: 46.94%

1 Month: 43.66%

1 Quarter: 39.11%

1 Year: 29.02%

5 Years: 10.82%

10 Years: 4.02%

20 Years: 0.67%

As the table shows, an investor who checks a US equity portfolio daily is likely to observe a loss roughly 49% of the time. Given the heightened intensity of negative emotions, frequent observers are going to experience much greater pain than joy from their investments. Even for those who review their portfolio just once a year, there remains a 29% chance of experiencing the pain of a loss.

Yet, if we introduce a 40% bond allocation to the portfolio, the probability of observing a 1 year loss drops to 26%. This slight reduction is often just enough to tip the emotional scales, making the overall experience positive and helping investors stay the course. Therefore, while a portfolio approach may be suboptimal for maximizing raw returns, it is far superior as a psychological vehicle to help investors actually reach their goals.

Mitigating the Unknowable

The second major benefit of a portfolio is that it mitigates the inherent uncertainty of investing. As humans, we love stories; when we look back at history, we easily construct a clear narrative explaining how we got to where we are today. Events that were shocking in the moment appear obvious with the benefit of hindsight. It is natural, though erroneous, to assume this predictable thread extends into the future, and that we simply need to work hard enough to unearth it.

Investors are not immune to this illusion (which partly explains the enduring enthusiasm for thematic investing). To be successful, however, we must acknowledge that the future is genuinely unpredictable. A vast spectrum of possible futures lies ahead, and our investment strategy must be able to encompass that uncertainty.

A diversified portfolio achieves this by combining assets that respond differently to the same economic forces. For example, energy companies surged following the onset of war in the Middle East, but they could be expected to deliver poor returns during a recession or a rapid shift toward alternative energy generation.

These diversification benefits, or, conversely, hidden concentrations, are not always visible using traditional risk assessment tools, which typically rely on historical relationships to predict the future. Therefore, it is critical to conduct scenario analysis, or ‘stress tests,’ to understand how a portfolio is likely to behave in specific environments and to make adjustments where significant vulnerabilities are discovered.

A prime example is provided by the growing influence of US technology stocks. Historically, Emerging Markets provided attractive diversification against a US equity portfolio. Today, however, because both the US and Emerging Markets are increasingly dominated by technology-driven companies, that historical benefit has deteriorated, forcing investors to look elsewhere.

Balancing Probabilities

It is important to note that this approach is not about eliminating all risk from a portfolio. Markets are reasonably efficient; investors who seek to strip away all risk through excessive diversification will inevitably receive substantially lower returns. The core process of investing is actively accepting some risk in exchange for higher expected returns.

The best way to balance the need to accept risk while insulating the portfolio against disaster is by applying probabilities to various scenarios. Scenarios that carry a high probability of occurring and imply significant losses must be addressed, while others can usually be ignored. A simple 2x2 grid is an effective tool for this exercise:

Cushioning Overconfidence

The third benefit of a portfolio approach is that it cushions our overconfidence, reducing the impact of inevitable analytical errors. While no one enjoys being wrong, mistakes are an inescapable part of investing and forecasting.

Despite this inevitability, most of us suffer from acute overconfidence, famously illustrated by Svenson’s research showing that 93% of American participants believed their driving skills were above average. In investing, this hubris often manifests as holding too large a position in a single asset, whether that is a specific company, a fund, or an entire asset class.

A well-structured portfolio requires clearly defined guardrails to limit the damage when our convictions prove misplaced. While standard in professionally managed portfolios, these limits are equally vital when managing your own money. They must be set at the beginning of the investing journey, as the temptation to break them is highest in the heat of the moment, precisely when markets are volatile and we are most vulnerable to making errors.

There have been many occasions throughout my career when rigid guardrails saved me from catastrophic mistakes when I was absolutely certain I had identified a terrific ‘opportunity’.

Because the benefits of strong guardrails are most apparent during market crises, they can be frustrating to adhere to during long periods of stability, when they inevitably hold back the returns of the portfolio. This drag is glaringly obvious when a prudently diversified portfolio ‘lags’ a highly concentrated benchmark or a risk-taking peer group.

It is much like paying for an insurance policy: it feels like a waste of money right up until disaster strikes. We struggle to visualize the counterfactual, easily ignoring the near-misses and averted disasters. Human nature makes us wish we only held insurance for the brief window when a crash is ‘guaranteed’. But we know that is not how insurance works; it must be maintained constantly to be effective. Similarly, portfolio guidelines must be applied continuously to protect our long-term objectives.

This doesn’t mean your rules should be entirely static; they must evolve over time alongside your experience, changing goals, and shifting market dynamics. By embracing this disciplined approach, you may occasionally underperform others when the investment weather is fair, but you vastly increase the likelihood of actually reaching your goals by smoothing the psychological challenges of investing.

Diversification may not be a free lunch, but it offers exceptional value and remains one of the most nourishing meals an investor can enjoy.

Dan - I can highly recommend the Fractals of Finance by Richard Brennan. It will challenge much standard thinking we have almost taken for granted. As he points out for example Markowitz had no interest in finance and his theory was a purely mathematical exercise regrettably based on false assumptions. Well worth a read there is much more in it than putting Marco out to grass!! All the best. Gandalf