The Portfolio Thinking Expected Returns Framework

A navigation tool, not a crystal ball

At the heart of every successful investment strategy is a set of expected returns. These can be derived in a number of ways with varying degrees of skill, however investing without them is like setting out on an arduous journey into an unknown country without a navigation aid. It is possible to reach your destination but it is unlikely to be a positive experience and may end in disaster.

In contrast, a well formulated set of expected returns can help us stay on the right path as we navigate challenging market environments by providing a consistent framework to guide our decisions and help us avoid being ‘whipsawed’ by changing market sentiment.

Before building model portfolios to express our investment views, we must create this framework. I’ve spent the last few months working on this and we’ll be publishing these expectations on a regular basis, but first, it is worth exploring their purpose and use of these expectations. While expected returns are required for all asset classes, this piece is focused on equities as these present the greatest challenge and opportunity for investors.

The Mirror and the Crowd

A common objection to expected returns is that they cannot consistently ‘outsmart’ the wisdom of crowds. While this is undoubtedly true, it misses the point. Our expected returns framework is not a crystal ball; it is an aid to decision-making. These estimates help us understand how our views differ from the consensus and, more importantly, what specific assumptions are “baked into” current prices.

Our approach is driven by the belief that capital markets are reasonably efficient over the long run and consequently capital tends to flow to where it receives the highest returns. While this flow of capital may be interrupted by barriers at the individual company level (described as Moats by Warren Buffett), these barriers tend to be less effective at a sector or market level and consequently, this continuous ‘tidal flow’ of capital is a powerful force that drives returns at the sector and market level back towards a long term average.

However, unlike the ocean tides that can be predicted with accuracy, capital markets comprise people who are subject to cognitive biases that can both create and sustain anomalies in the flow of capital and hence implied expected returns for months or even years.

The Shiller Underpinning

While these anomalies in any single market are rarer than many active managers would like to admit, across global capital markets, there are often asset classes which investors are treating with an unusual degree of pessimism or optimism. Evidence for this view is provided by Robert Shiller’s Nobel lecture in which he demonstrated that prices of US equities frequently depart from the ‘correct’ price, that is, the value that investors with perfect foresight would assign to the market. While most of these departures are simply noise, some are sufficiently large to bolster the returns to investors prepared to own unpopular assets and conversely suppress returns to those assets that have attracted too much capital and optimism..

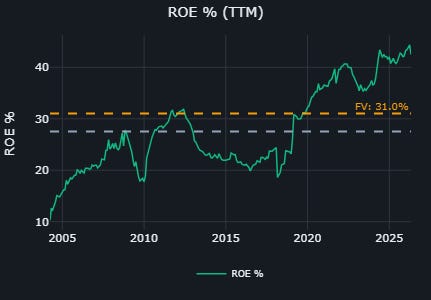

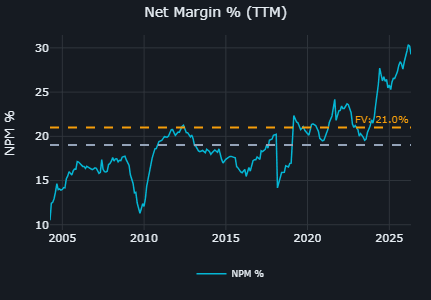

Case Study: The Weight of Optimism in US Technology

The most obvious example today is the US Technology sector. The following charts show the historic net profit margin, return on equity and precise earnings ratio for that sector.

Source: Morningstar Data 30th April 2026

In the heat of a fundamental technological shift, it is difficult to imagine any outcome other than the dominant narrative that these metrics will stay at the current elevated levels or rise even higher. However, it is precisely this lack of imagination that creates valuation anomalies.

If these metrics were to return to normal levels, a move consistent with the long-term “tidal flow” of capital, it would act as a massive headwind. Our framework suggests a potential valuation drag of nearly 3% per year over the next decade for the sector.

The Challenge of Forecasts

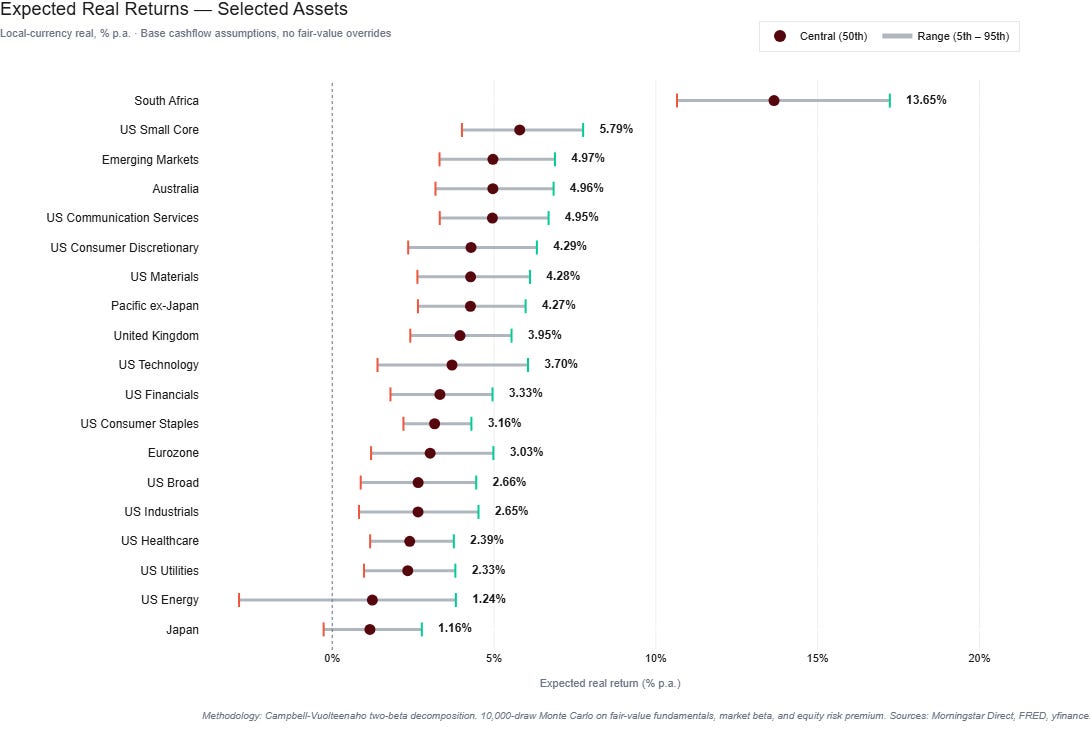

Because we lack a crystal ball, expressing expected returns as a single “point forecast” is a recipe for overconfidence and error. A single number implies a level of certainty that simply does not exist in human systems.

For this reason, we express our expected returns as a distribution of possible outcomes. While it is impossible to fully encompass the uncertainty of the future, this approach can help us identify where the expected returns between two assets are genuinely different or overlap so greatly as to make differentiation meaningless. An example of this output can be seen below.

These expectations are tools to help us think through the challenge of investing. They provide the navigation aid that allows us to distinguish between the destination and the distractions. They are not an accurate guide to the future, but a disciplined way to prepare for it. Like all tools, they must be used carefully, with a focus on stewardship rather than prophecy.